SAN DIEGO — Seniors housing’s standing in the investment world is on the rise, says Lisa McCracken, head of research and analytics at the National Investment Center for Seniors Housing & Care based in Annapolis, Maryland.

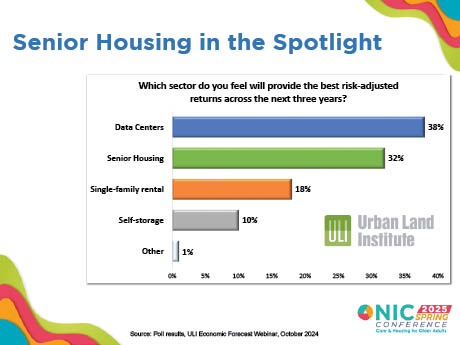

During a webinar hosted by the Urban Land Institute in October 2024 highlighting its real estate economic forecast, the organization polled over 2,000 registrants on the following question: “Which sector do you feel will provide the best risk-adjusted returns across the next three years?”

Data centers captured the largest share of responses (38 percent), followed by seniors housing (32 percent), single-family rental properties (18 percent), self-storage (10 percent), and other (1 percent).

“We were second behind data centers, and data centers are pretty sexy right now, right?” said McCracken. She noted that seniors housing professionals accounted for a small portion of the ULI webinar registrants, making the results even more impressive.

The anecdote shared by McCracken came Wednesday, March 5, during a panel session she moderated on the opening day of the NIC Spring Conference taking place at the Marriott Marquis San Diego Marina. Approximately 2,060 industry professionals have registered for the event, setting a new record for the spring conference, according to NIC. Of that total, 470 are first-time attendees, many of whom work on the capital side of the business.

McCracken’s panel, titled “What a Difference a Year Makes — Senior Housing Capital, Investment & Growth Outlook,” included Thomas Errath, managing director and head of research for Harrison Street; Arick Morton, CEO of NIC MAP; and Jamie Woodwell, head of commercial real estate research for the Mortgage Bankers Association.

Institutional Investors Take Note

Harrison Street is an investment management firm focused exclusively on alternative real assets. Since its inception in 2005, Harrison Street has invested across seniors housing, student housing, build-to-rent, healthcare delivery, life sciences and storage real estate. The firm has $56 billion of assets under management.

“Part of the reason our firm invests in seniors housing is it has this demographic thesis to it,” explained Errath. Regardless of the health of the economy or what’s occurring with interest rates or policy coming out of Washington, D.C., seniors still need this product, he emphasized. “They might need it in a different way. They might spend more; they might spend less.”

Other real estate sectors that Harrison invests in are experiencing strong rent growth, like what’s been taking place in seniors housing. The difference is that the occupancy rate in most of these other sectors is the mid-90 percent range. The seniors housing occupancy rate for the 31 primary markets tracked by NIC MAP was 87.2 percent in the fourth quarter of 2024, surpassing pre-pandemic occupancy levels, but that still pales by comparison.

That 87.2 percent figure has piqued the interest of institutional investors because given the strong consumer demand for seniors housing and the limited new supply coming online, there is strong reason to believe that the occupancy figure will only increase over the next few years, said Errath.

Rising labor and materials costs have been an impediment for general contractors and developers over the past few years, Errath noted. The 25 percent tariffs imposed by the U.S. on nearly all goods from Mexico and Canada that officially went into effect on Tuesday, March 4, aren’t helping matters. The U.S. imports a significant amount of lumber from Canada and drywall from Mexico.

“So now there is even more fog in the equation,” said Errath. “I think it’s going to be tricky to do some new [construction] starts. You’re going to have to be in the kind of market where you think you can rally to a pretty high rental rate to get there.”

GSEs Under the Microscope

The future of Fannie Mae and Freddie Mac remains a hot topic. The two giant government-sponsored enterprises (GSEs) were placed in conservatorship by the Federal Housing Finance Agency (FHFA) in September 2008 to stabilize the financial markets amid the housing market crash.

Fannie Mae and Freddie Mac’s total assets at the end of 2024 were $4.3 trillion and $3.3 trillion, respectively. Mortgages account for a large portion of those total assets. McCracken asked MBA’s Woodwell, who is based in Washington, D.C., what the impact would be if the two entities were released from the government into the private sector.

“There are some significant downsides to them being in conservatorship,” said Woodwell, who didn’t elaborate on the negatives. Proponents of privatizing the GSEs say it would promote competition in the mortgage market and shift risk away from taxpayers.

“If you look at the Trump 1.0 administration, it put in place a number of steps to get the GSEs on the path to exit conservatorship: a new capital regime, retaining capital, other things like that,” noted Woodwell. During the Biden administration, any momentum to privatize the GSEs shifted amid the FHFA’s changing priorities.

“So, there was an expectation that with the Trump administration coming back in, it would pick up the ball and start moving forward,’’ said Woodwell.

However, the new administration has been sharply focused on extending the Tax Cuts and Jobs Act of 2017. Many provisions of the act are set to expire at the end of this year. “One of the big activities for Congress this year is to figure out how to extend or make those cuts permanent,” said Woodwell.

The veteran researcher, who worked on MBA’s first effort 17 years ago to get the GSEs out of conservatorship, believes it’s imperative that several important steps be taken before they are taken private — the biggest of which is an “explicit backstop” on the mortgage-backed securities they issue.

Legislators on Capitol Hill and members of the Trump administration have widely acknowledged the importance of executing these steps as a precursor to taking the GSEs private.

“While there have been times when you think, ‘Wow, this could really happen quickly,’ we’re getting back to the fact that there needs to be a thoughtful process to get them out [of conservatorship], and that might take a number of years to do,” said Woodwell.

It’s a very fluid environment in Washington, D.C, observed Woodwell. “Our hope and expectation is that there’s a deliberate process to say what really needs to be in place at the end of the day when they come out of conservatorship to make sure that they continue to support the [housing] market.”

— Matt Valley