By Jane Adler

Private equity firms are snapping up a bigger slice of the seniors housing market as investors seek healthy returns. The rationale for investing is increasingly clear: The long-anticipated baby boomer wave is arriving, bringing a growing need among these older adults for more appropriate housing and expanded care options.

Seniors housing occupancies and rental rates are rising. New development is still constrained. And other commercial real estate asset classes are not performing as well as seniors housing, which is generating decent returns.

Given these dynamics, it’s not a surprise that capital is pouring into the sector. New private equity firms are being formed. Established funds that once overlooked seniors housing are buying properties, and long-time players are expanding their portfolios.

Competition for newer, high-quality properties is increasing. Valuations are up. Cap rates are down.

Meanwhile, investment strategies are beginning to pivot away from value-add opportunities toward core assets that offer more stable, predictable returns.

Real estate investment fundraising is rebounding, according to Preqin, a London-based global provider of data, analytics and insights for alternative assets such as private equity and real estate, that is owned by New York City-based asset manager BlackRock.

Global real estate fundraising totaled $127 billion during the first three quarters of 2025, nearly matching 2024’s full-year total. North America-focused private real estate fundraising, which includes funds with an emphasis on seniors housing, reached $27.2 billion in 2025.

“There is absolutely more money flowing into seniors housing,” says Rick Swartz, co-head of senior housing at JLL, who is based in the firm’s Boston office. “Private equity firms are raising funds to invest in properties.”

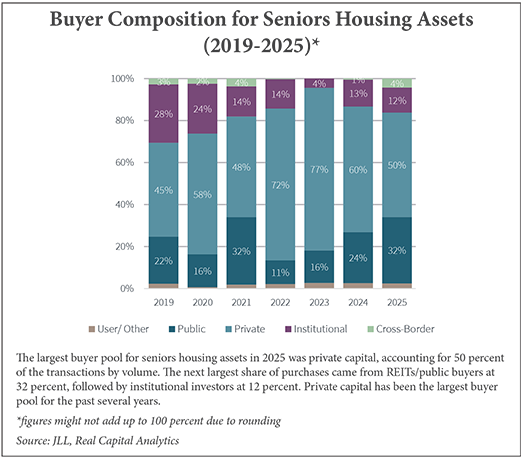

The seniors housing sector experienced its strongest year in a decade, with rolling four-quarter transaction volume reaching $24 billion by year-end 2025, the highest level since the second quarter of 2015, according to JLL’s “2026 Seniors Housing & Care Investor Survey and Trends” outlook. Private capital accounted for 50 percent of transactions by volume.

Alongside student housing and medical office, seniors housing ranks among the three largest alternative sectors in terms of investment volume, the JLL report says.

The alternative sectors collectively accounted for 16.2 percent of all commercial real estate

dollar volume in 2025 — higher than its prior peak of 13.1 percent in 2017.

Investors are continuing to raise capital to deploy into these smaller sectors, which in many cases offer greater growth prospects than the main asset types, the report states.

Private equity firms, which typically have a hold period of five, seven or 10 years, are backed by a mix of institutional and private capital, including pension funds, endowments, sovereign wealth funds, high-net-worth individuals and family offices.

Firms Weigh Next Steps

Amid changing market conditions, private equity firms are fine-tuning their seniors housing strategies.

Chicago-based Harrison Street Asset Management is the fourth largest owner of seniors housing properties in the U.S., according to the latest rankings by the American Seniors Housing Association.

Colliers International Group Inc. (Nasdaq: CIGI) acquired a 75 percent stake in Harrison Street for $550 million in 2018.

Harrison Street launched its seniors housing investment strategy in 2005. During the past two decades, the firm has invested in more than 40,000 seniors housing units nationwide. The firm owns seniors housing communities within its opportunity funds, core fund and separate accounts.

Harrison Street has also been building a credit strategy that will target opportunities to originate loans backed by seniors housing assets.

“Given our long-term conviction in the sector, we have created diversity in capital, ranging from opportunistic to core, as well as both equity and credit,” says Mike Gordon, global chief investment officer at Harrison Street.

The company is focused on growing its seniors housing strategy alongside approximately 15 operating partners.

For example, Harrison Street has partnered with Belmont Village Senior Living on a number of projects over the years. A recent Belmont Village development is underway in Encinitas, California. The site near San Diego is a former strawberry field that was in the entitlement process for several years.

“It’s an example of the investments that we’ve made in high-barrier, unique micro markets,” says Gordon.

He explains that the firm employs an investment strategy that involves analyzing sites through a proprietary zip code qualified market screen that is informed by decades of investing experience and substantive internal data that the firm has accumulated over the course of the firm’s 20-year history.

Promising locations are identified and matched with Harrison Street’s operating partners. “We look at dozens of market, operational and asset-level metrics,” says Gordon.

“It requires a tremendous amount of time, work and perseverance to create shovel-ready projects in these coveted micro markets. However, once an asset is built and stabilized, the nuances of these markets can drive really strong revenue growth and net operating income (NOI) margins, and this profile of trophy asset is becoming increasingly attractive to a broadening universe of players across the capital markets,” explains Gordon.

Rather than a wholesale strategic shift,

Gordon describes the firm’s approach as a continuous sharpening of focus.

“We’ve spent 20 years building conviction in sectors where demand is demographically inevitable and operationally complex, and seniors housing sits at the center,” he says.

“We’re harnessing a tremendous amount of data and experience, and we’re more concentrated today with certain long-standing

operating partners than we were 10 years ago. This is a byproduct of our lessons learned. But our convictions have never been stronger with respect to seniors housing,” adds Gordon.

Private equity real estate investments are generally categorized into three strategies based on risk-return profiles: core, core plus and value-add.

Core investments offer low-risk, stable income from stabilized properties in prime locations with expected levered returns of 6 to 10 percent annually.

Core-plus investments offer moderate risk to gain higher returns through minor improvements with expected levered returns of 8 to 12 percent annually.

Value-add investments involve substantial renovations or operational changes for high growth with expected annual levered returns of about 15 percent or higher. Over the last 24 months, many private equity investors have often been seeking value-add type properties, sources say.

The investment thesis has been that these communities, many of which are still struggling in the aftermath of the pandemic, could be repositioned to boost occupancies, improve NOI, and generate outsized returns of about 15 to 20 percent. But that pool of opportunities is shrinking.

A Change in Strategy

The investment market is shifting, according to Brian Sunday, managing director and portfolio manager of seniors housing at Boston-based AEW. The firm owns 70 senior living properties with about 10,000 units and works with 18 operators.

“We tend to focus on newer vintage properties with a continuum of care,” says Sunday.

Demand for older properties has weakened, while newer assets are drawing significant interest, attracting 10 or more bids, according to Sunday. These properties offer the modern amenities and larger units preferred by baby boomers.

“Everyone is targeting the same assets,” he says.

Competition for newer properties is increasing valuations, compressing cap rates and lowering potential returns. Sunday notes that while private equity has recently achieved levered returns of 15 percent or more, those returns are now tightening.

“Can capital stomach returns in the low teens?” he asks. “That’s where the market is shifting and shifting fast.”

As a result, AEW is looking at ground-up development deals. “There are a few markets where development is starting to look attractive,” says Sunday. “When we do start developing again, we want to be early in the cycle.”

Other investors are adjusting their strategies. The private real estate investment arm of Morgan Stanley is fine-tuning its approach as senior living fundamentals improve.

“Earlier, we identified the sector as an opportunity,” says Will Milam, head of U.S. investments for Morgan Stanley Real Estate Investing based in New York City.

In 2022, as the sector continued to face challenges from the pandemic, Morgan Stanley bought the Arbor Spring portfolio. Property performance gradually improved and Morgan Stanley sold the portfolio of 11 properties in Maryland and Virginia for $296 million in February 2026. Ventas, the giant healthcare REIT, was the buyer, according to published reports.

“We’re being very selective,” says Milam, about the firm’s current acquisition strategy. “We’re targeting Class A, high-performing assets to capture outsized rent growth.”

In December, Morgan Stanley closed a $305 million acquisition of a three-property portfolio in the Denver area from Kayne Anderson. The communities are managed by MorningStar Senior Living, which will continue as the operator.

“This transaction fits with our investment strategy of partnering with best-in-class

operators to acquire high-quality communities with a continuum of care and modern amenities,” says Milam. “Our investment thesis is to grow NOI. We continue to see the best risk-adjusted returns with Class A properties.”

Niche Opportunities, New Entrants

Value-add properties remain in play, though attractive deals are becoming harder to find. Fortress Investment Group adopted a value-add strategy in 2021 at the onset of the COVID outbreak.

“We saw an industry in seniors housing with real short-term challenges but a great long-term outlook,” says Pete Stone, head of healthcare real estate equity at Fortress in Dallas.

“So, we started to acquire assets that we could improve operationally and physically to drive a better resident experience. Our view was that there was a great silver lining of demand going forward, and that scenario has transpired.”

Stone says the firm built an integrated team to handle acquisitions, asset management,

construction and operations. “That allows us to buy assets we think we can improve,” he says.

Since 2021, the firm has invested in 15 properties. One example is Andara Senior Living, a 170-unit senior living property offering independent living and assisted living in Scottsdale, Arizona. The property was built in 2010, and few improvements had been made over the years. “The property was dated,” recalls Stone. “It had an

art deco feel.”

A $5 million renovation focused on creating a more contemporary environment. Memory care units were added to the community, and amenitie, including the bistro, common areas, theater, library and fitness space, were upgraded.

“Baby boomers are looking for a more amenitized building,” says Stone.

Renovations were completed at the end of 2025. Cogir Senior Living is the operator. “The goal is to improve the asset, drive occupancy and to institute meaningful rent increases associated with the renovation,” says Stone.

Similarly, Focus Healthcare Partners targets repositioning opportunities.

“We’ve gotten comfortable doing transformational deals,” says Mike Feinstein, a managing director at the Chicago-based firm, which currently owns 24 properties and is now investing its third institutional equity fund.

Four buildings have already been identified for the new fund and Feinstein expects to add up to 30 more. Focus works with operators across the country.

“We like large buildings,” says Feinstein of the firm’s strategy. Big buildings with 200-plus units offer the opportunity to provide consumers with a solid range of options.

“The continuum fills multiple needs for residents and their families over time,” he says, adding that about 70 percent of the units in the Focus portfolio are independent living apartments.

In 2023, Focus purchased Lexington Square Senior Living in Elmhurst, Illinois, a western suburb of Chicago.

The community, which was owned by a private family, was built in 1990 and has 329 units. The property has been rebranded as The Roosevelt at Salt Creek and converted from an entrance-fee, buy-in model to a rental community.

Following a nearly $30 million renovation, the property now features expanded dining venues, a club room, sports bar, and coffee shop, along with 19 new memory care units that leased within six months. As of press time, the grand reopening of the community was scheduled for April 23, 2026.

Life Care Services is the operator of The Roosevelt at Salt Creek. Occupancy has increased from approximately 40 percent at acquisition to 80 percent today.

“We’ve built a strong team,” says Feinstein. “It’s one of the best renovations, offering a great acuity mix at rents that are competitive or below other buildings in the market.”

A one-bedroom unit costs $4,495 a month and includes meals, transportation, housekeeping and robust lifestyle programming.

Meanwhile, new private equity firms are also entering the market, often headed by industry veterans.

A former executive at Artemis Real Estate Partners, Kelly Sheehy, launched Atlanta-based Arcole in December 2025 along with capital partner Town Lane, a New York City-based real estate manager. Sheehy is founder and managing partner at Arcole.

Arcole recently closed on the acquisition of The Sheridan at Green Oaks, a 198-unit independent living, assisted living and memory care community in Lake Bluff, Illinois, a suburb of Chicago.

AEW was the seller and Solera Senior Living is the operator. The community, built in 2016, is being rebranded as Modena Green Oaks. It is 87 percent occupied.

“This is a value-add investment,” says Sheehy. The purchase price was not disclosed, but Sheehy says the sale was the result of a competitive bidding process.

Sheehy’s plan is to execute a multimillion-dollar refresh of the property and improve operations. He also plans to build 20 new 1,800-square-foot duplex cottages on the 17-acre site.

“I’ve tracked this building’s progress since it was developed,” says Sheehy. “We see upside on operations in partnership with Solera.”

Eight Factors New Entrants to Seniors Housing Need to Consider

Despite the strong investor enthusiasm for seniors housing, industry veterans caution that it’s a complex landscape to navigate, particularly for new entrants to the sector. Here are eight factors currently weighing heavily on the industry.

Operationally intense: Senior living requires more hands-on management than other asset types. Residents typically need some type of care, and in some cases health care, not just housing. “Groups without the experience to deal with the operational challenges can find the sector difficult,” cautions Kelly Sheehy, founder and managing partner at Atlanta-based Arcole, a private investment firm.

High staffing requirements: Labor demands far exceed other commercial property types. A 100-unit assisted living building can require 50 to 80 workers.

Worker shortage: The senior living industry faces a workforce shortage. The turnover rate of employees is high, about 35 to 45 percent annually. The pool of available workers is shrinking.

Hard to scale up: Rapid expansion is difficult. “The fundamentals are great, but scaling up without making mistakes is not easy,” says Brian Sunday, managing director and portfolio manager of senior housing at Boston-based AEW.

Competition: Many investors chase the same types of best-in-class, newer properties, which is pushing up values and potentially decreasing returns.

Functionally obsolete buildings: The average seniors housing building is 24 years old. It can be difficult to reposition many of these buildings that lack the amenities sought by today’s residents. Some buildings have a number of studio apartments that are difficult to lease.

New construction: “Keep an eye on new construction,” says Rick Swartz, co-head of seniors housing nationally at JLL who is based in the firm’s Boston office. New projects take several years to develop, but when completed they can take pressure off the significantly undersupplied markets.

Affordability: While the industry searches to find a way to make senior living more affordable to a broader group of people, rising costs are making senior living less affordable for many people.

— Jane Adler

— This article originally appeared in the April 2026 issue of Seniors Housing Business magazine.